Capital Allocation at Altria

Capital Allocation at Altria

Much more good than bad.

If you take one lesson away from this piece, let it be this:

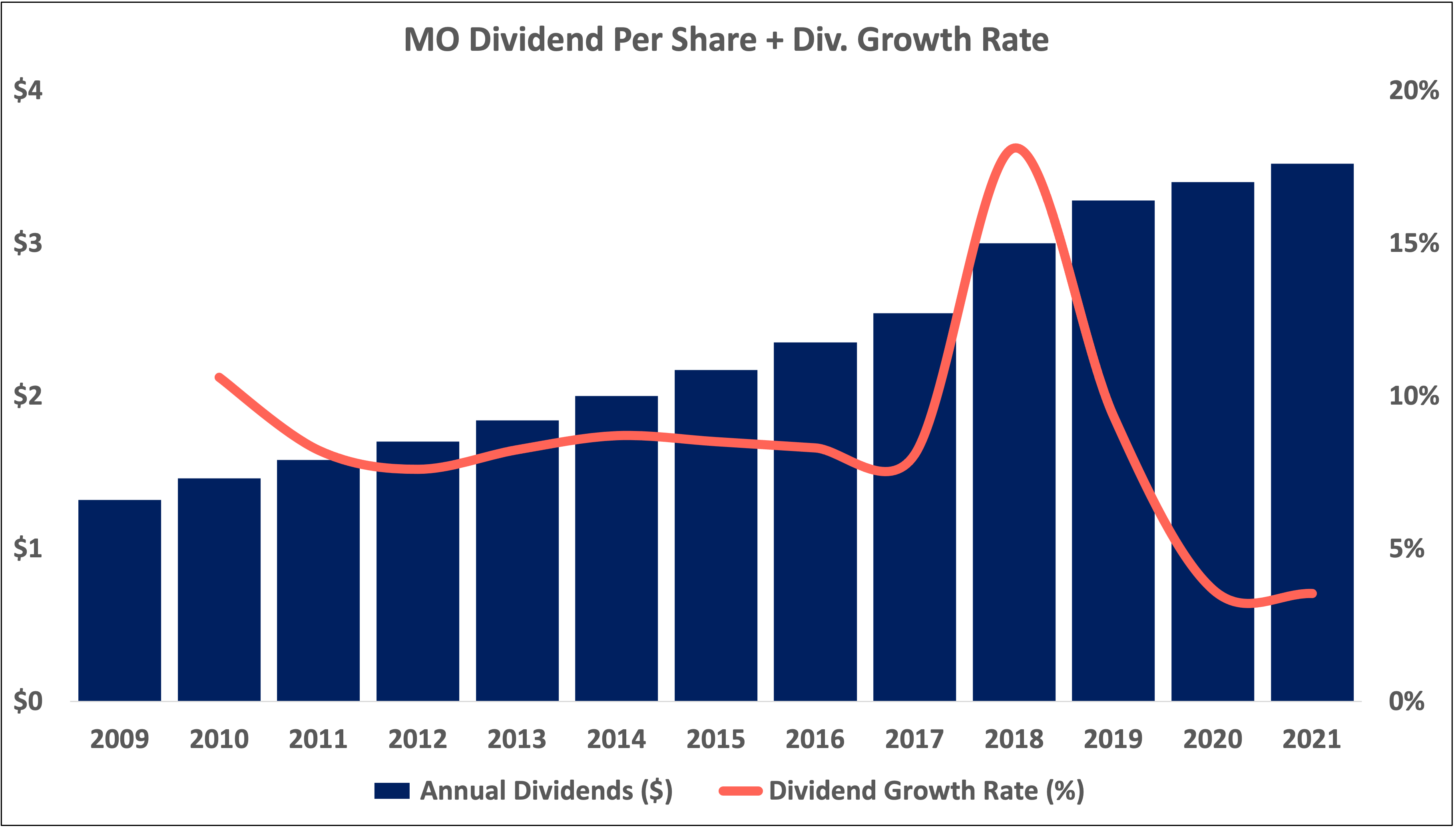

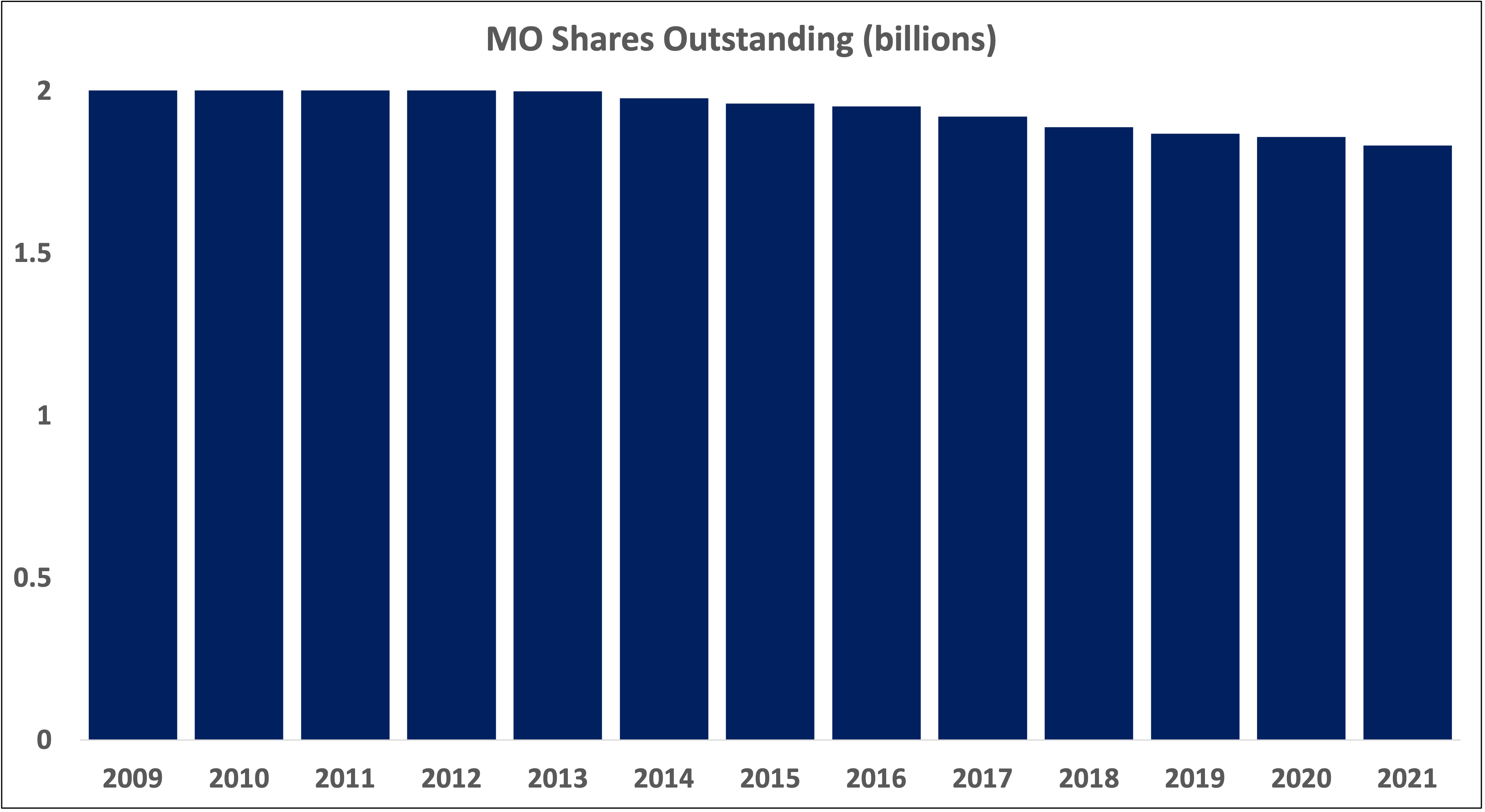

Put another way: Altria’s market capitalization today is $84 billion. So from 2009 to 2022, management has dished out ~90% of the value of the company to shareholders via dividends and buybacks (the company reduced its share count by over 11% between 2009 and 2021).

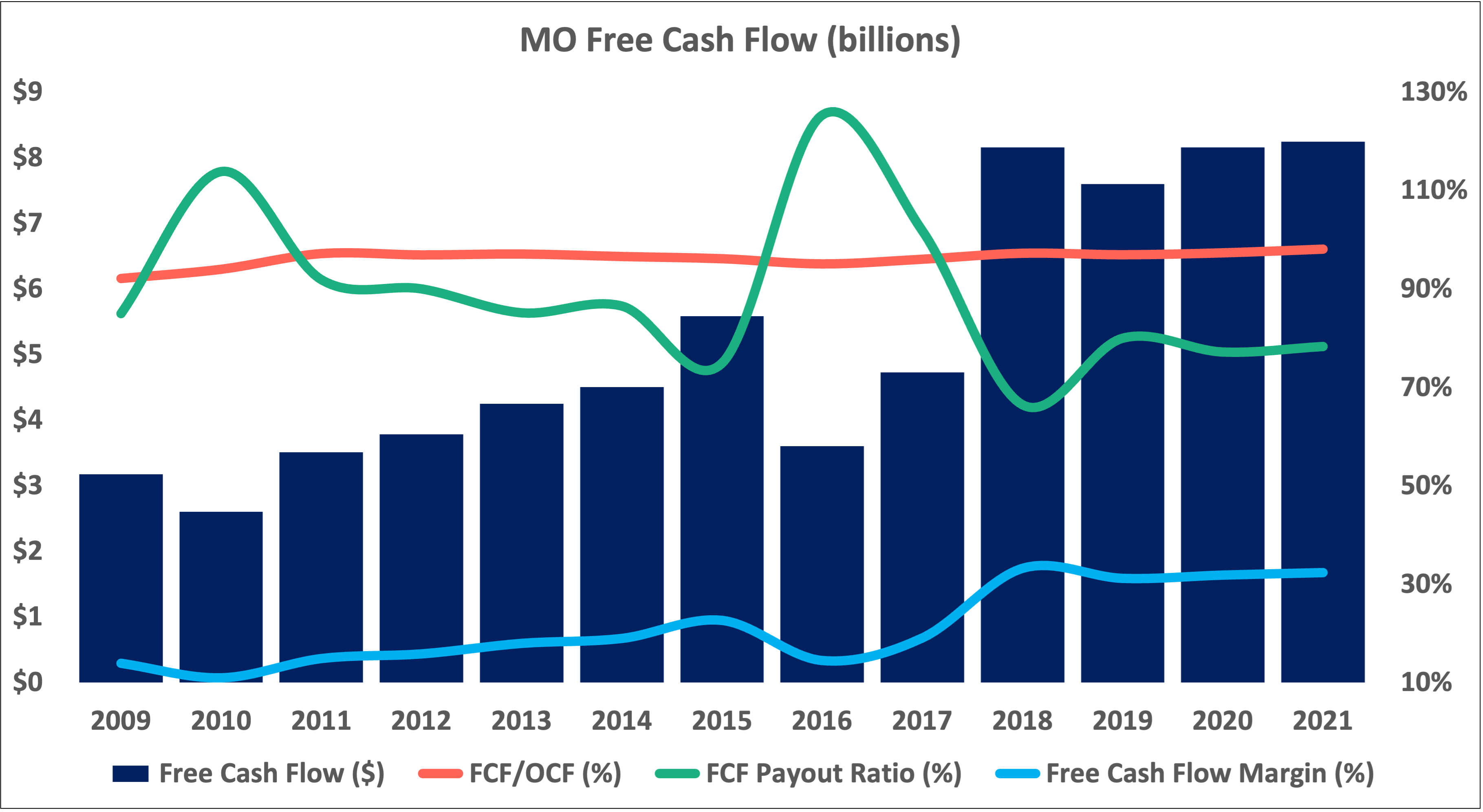

Relative to operating cash flow, Altria’s business spends very little on CAPEX. Since 2009, Altria’s average annual spend on maintaining, buying, and improving its fixed assets — properties like factories and equipment — has amounted to less than 5% of operating cash flow. Not many businesses can claim to convert over 95% of operating cash flow to free cash flow for over a decade.

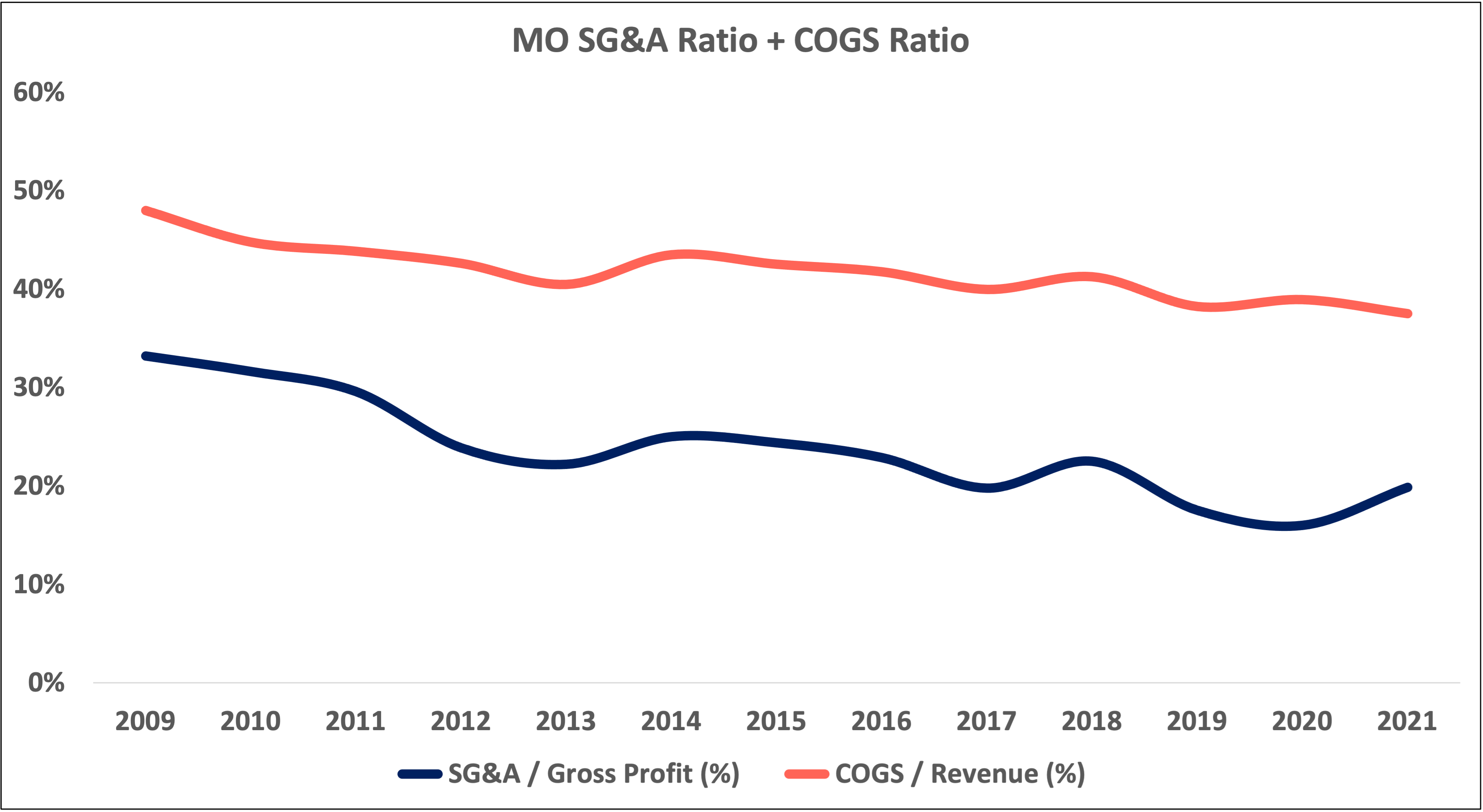

Altria is able to generate the cash flow needed to pay out dividends and repurchase shares because of management’s ability to control costs. While Altria’s nicotine revenue is up almost 12% from 2009 to 2021, its cost of goods sold (COGS — i.e. the costs of the materials and labor needed to manufacture cigarettes and other products) has dropped over 12%.

And while gross profits are up almost 60% over the same period, Altria’s overhead (known as SG&A — i.e. salaries, rent, sales force costs, distribution costs, etc.) has declined over 5%.

Against this backdrop of strong free cash flow and exemplary capital allocation and cost control, management’s $12.8 billion and 1.8 billion investments in Juul (2018) and Cronos (2019), respectively, don’t seem too bad.

Thanks for reading.

Other pieces in this series on Altria: