The New and Improved Philip Morris International

The New and Improved Philip Morris International

Volume growth is the new norm.

PMI’s share price is up 29% from 2012 to 2022. The S&P rose 224% over the same timeframe. The market has shunned Big Tobacco because of (1) falling volumes and (2) the ethics around investing in companies that sell deadly products. Despite these past problems, PMI’s future looks great.

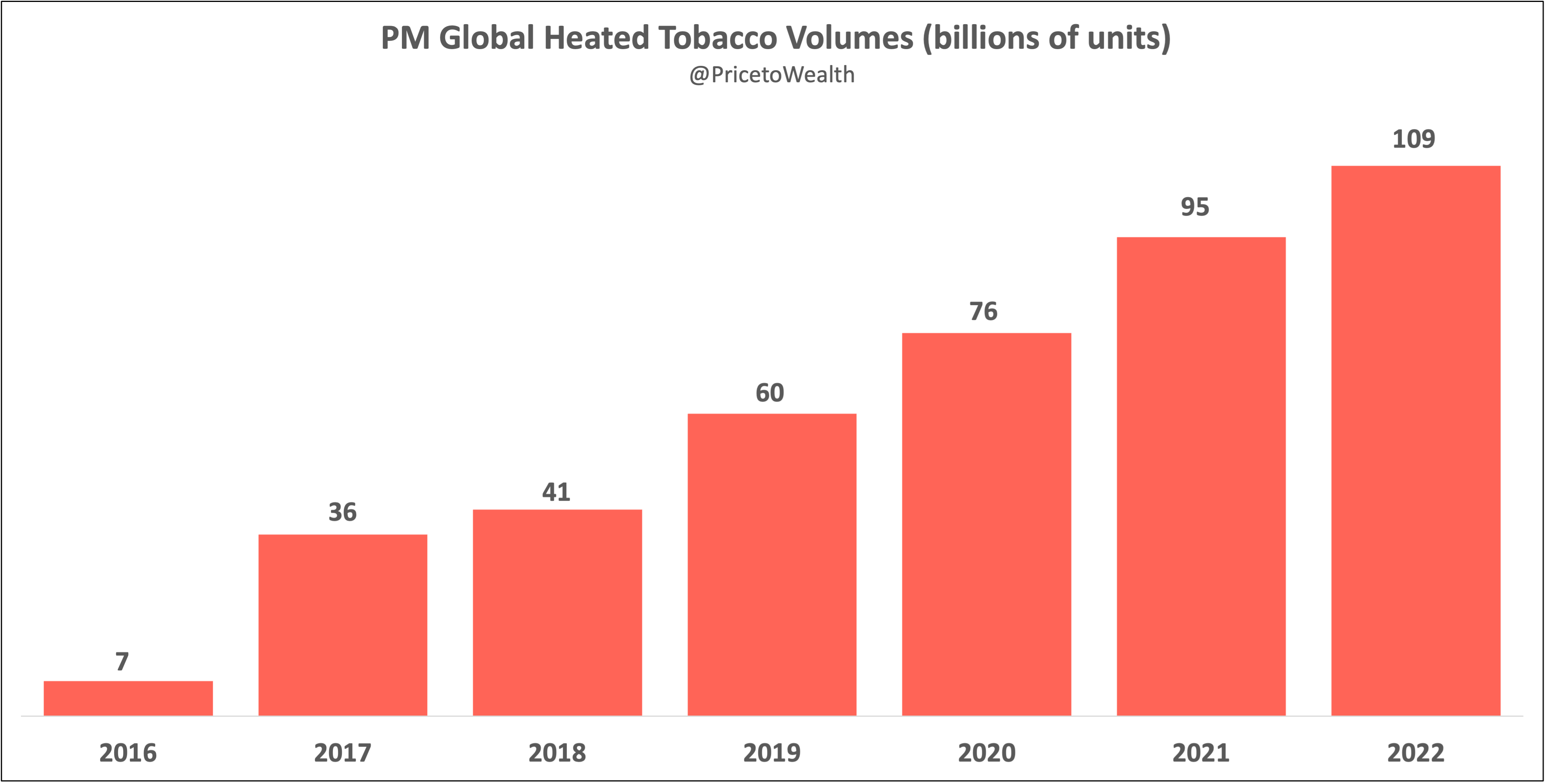

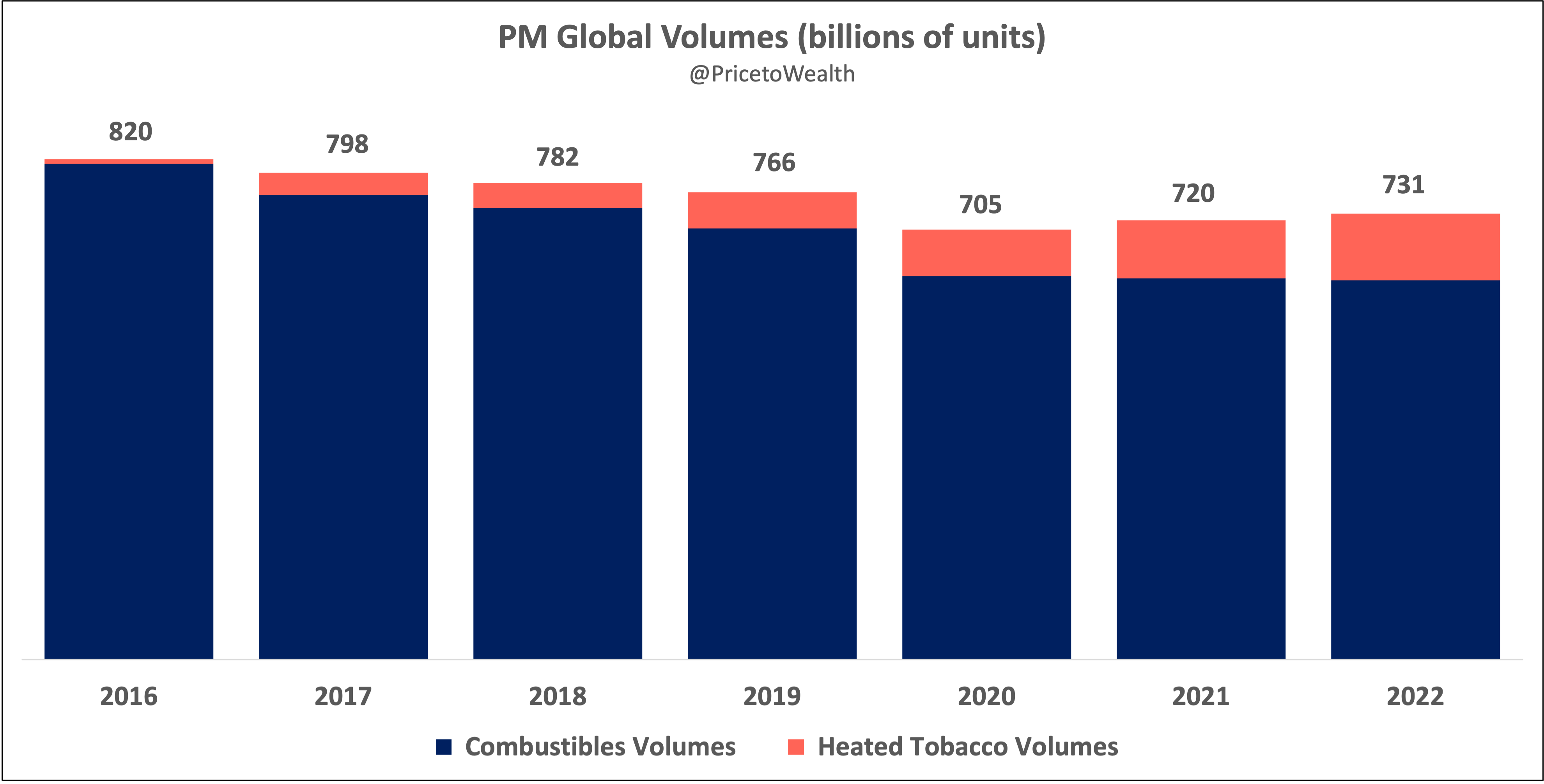

Without abandoning its cash-cow cigarette business, PMI has pivoted to selling reduced-risk nicotine products. It’s going well. Reduced-risk (i.e., heated tobacco) volumes are up almost 1600% from 2016 to 2022. Total volumes are up almost 4% from 2020 to 2022. Combustibles are almost flat over the same timeframe.

This turnaround in volumes suggests that the global nicotine market could be growing rather than shrinking. Another explanation: PMI is taking share from its competitors. Either way, PMI is the opposite of a melting ice cube. In fact, PMI has been growing revenue since 2016 when it started heavily promoting a smoke-free future centered on its reduced-risk products (RRPs). Smoke-free revenues now account for a third of PMI’s top line.

Operating income is starting to take off too. Though, it would be reasonable to expect some fluctuation in that department as PMI works through losses relating to the Russia/Ukraine conflict, the Swedish Match acquisition, RRP development costs, and management’s continued investment in the company’s new “wellness and healthcare” segment. Yes, despite the irony, management claims to be staking at least a part of the company’s future on healthcare products. We’ll see where that goes.

Overall, given the turnaround in volumes, PMI is well-positioned for growing profits over the long term. After years of developing and promoting its lineup of reduced risk products, it looks like management’s long game is paying off.

Thanks for reading!