Philip Morris International: Americas

Philip Morris International: Americas

A snapshot of PMI's most exciting market.

The United States 🇺🇸, Canada 🇨🇦, Mexico 🇲🇽, and the many countries of Central and South America (plus the Caribbean) make up PMI’s Americas market. The Americas account for just 6% of PMI’s revenues and 3.5% of its operating income. PMI does not sell cigarettes in the U.S. (Altria has the rights to Marlboro et al. in the U.S.).

Roughly 12% of American adults smoke. That’s ~30 million smokers. Management no doubt sees those ~30 million as an opportunity to substantially increase its IQOS user base. For some perspective, there are ~35 million smokers in France and the U.K. combined, where about 33% and 15% of adults smoke, respectively.

17.5% of Canadians smoke. ~7 million smokers.

13% of Mexicans and Brazilians smoke. ~44 million smokers.

25% of Argentinians smoke. ~11 million smokers.

Litigation in Canada has made PMI’s Americas business look bad on paper. PMI lost a litigation battle in Canada against Canadian smokers who claimed damages from smoking PMI’s products. A Canadian court granted PMI’s subsidiary there creditor protection, which required PMI to deconsolidate its Canadian subsidiary. Thus, PMI cannot include in its financials any of the revenue, operating income, etc. earned by its Canadian subsidiary until management reaches a settlement with its creditors there.

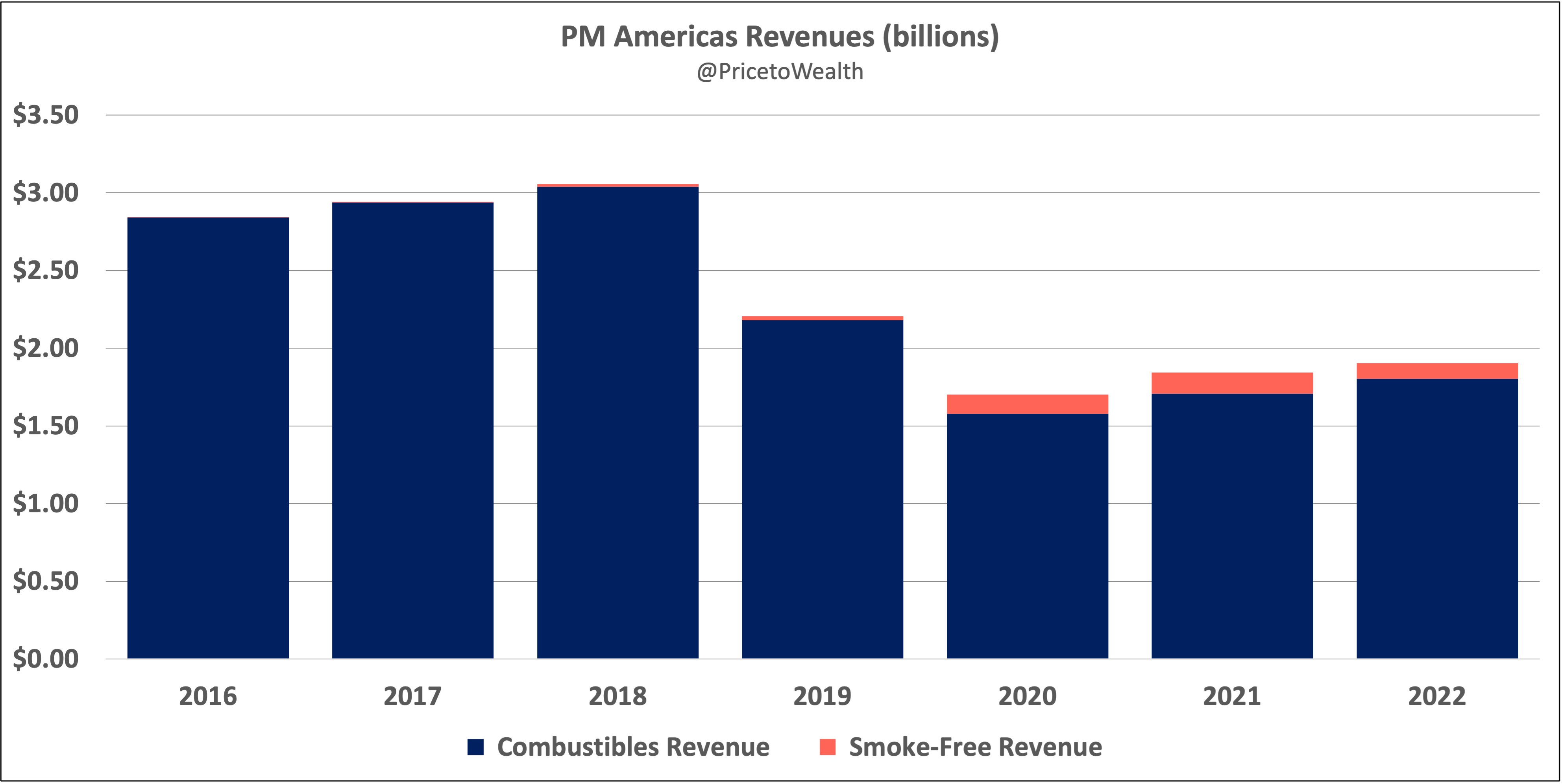

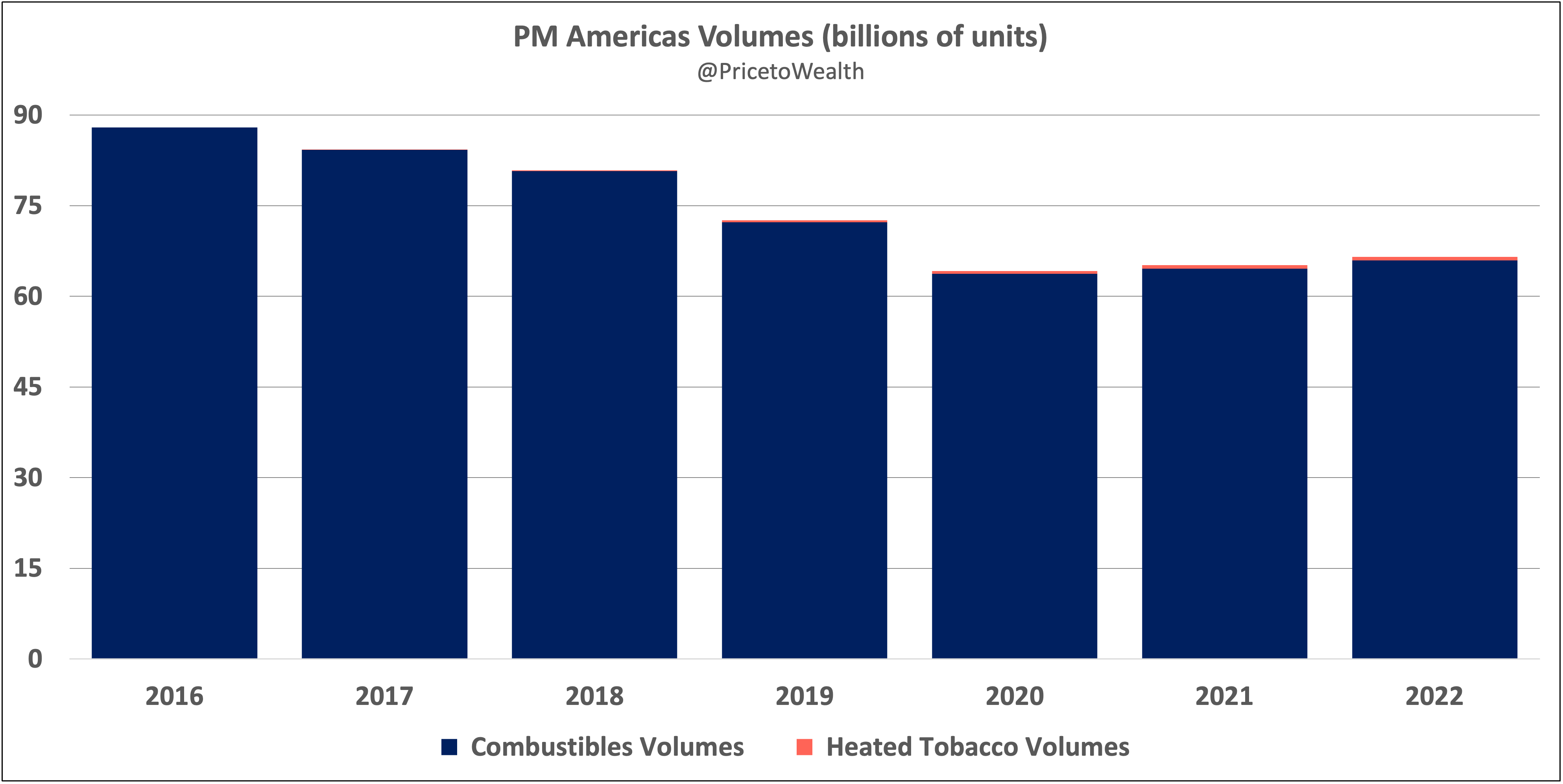

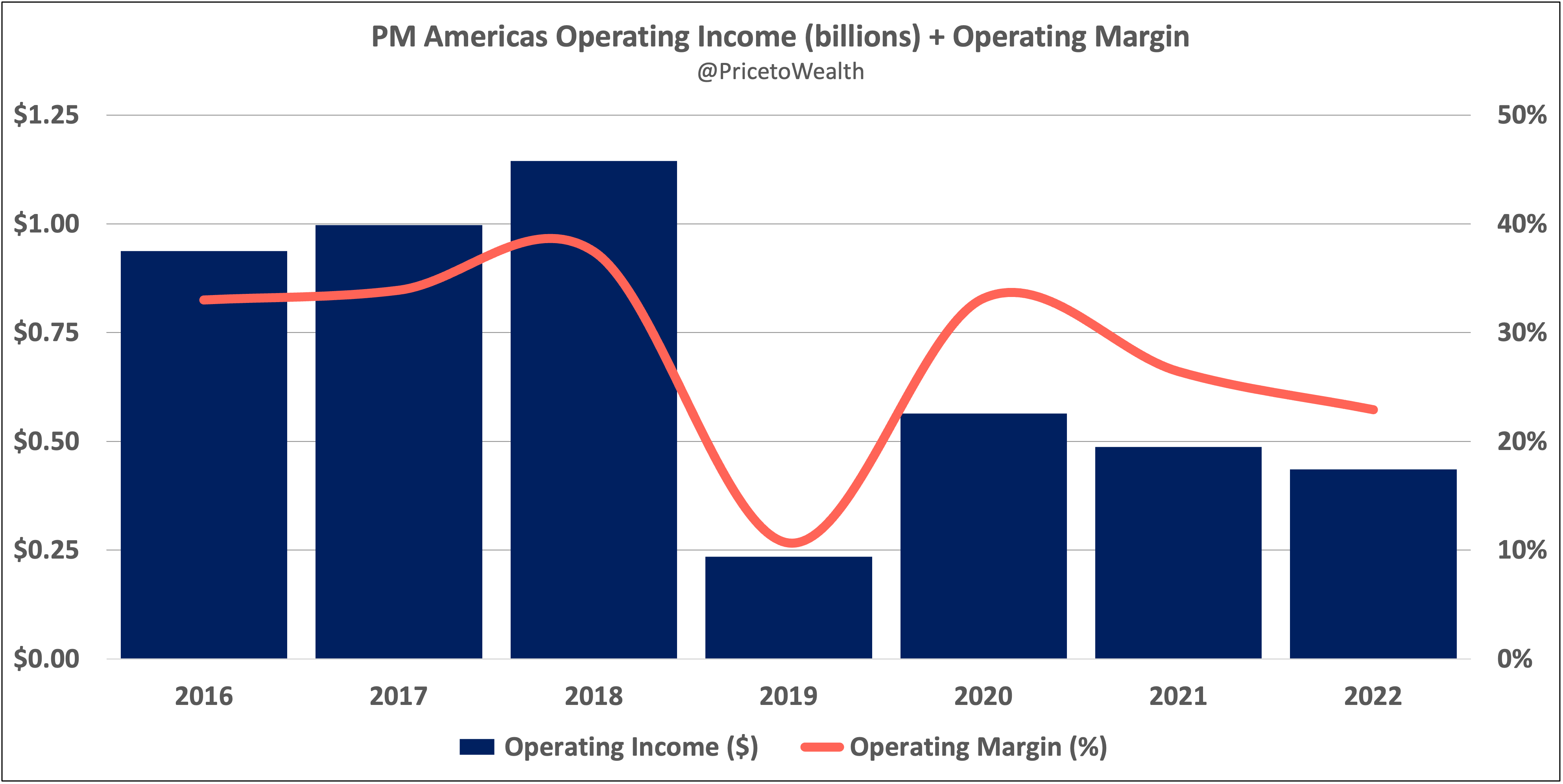

As a result of the deconsolidation of its Canadian subsidiary, revenue, volumes, and operating income from the Americas are down 33%, 24%, and 54%, respectively. Smoke-free revenue accounts for just 5% of total revenues in this market, while heated tobacco accounts for less than a percent of volumes.

Despite this superficial underperformance, under the hood, PMI’s Americas business actually looks not too bad. First, with smoke-free’s share of revenue sitting at just 5% in the Americas, PMI has a lot of opportunity to grow that side of its business. Second, pre-deconsolidation (2016-2018), revenues and operating income were up 8% and 22%, respectively. Volumes were down 8%. And third, post-deconsolidation (2020-2022) revenues have grown 12%, with volumes up 4%. Due to a tax credit in Brazil, rising manufacturing costs, charges relating to the Swedish Match acquisition, and higher administrative, marketing, and research costs, operating income in the Americas has trended down 23% post-deconsolidation.

Looking ahead several years, for those who can get FDA authorization, there’s a lot of opportunity for sellers of non-combustibles in the States. PMI’s imminent entry into the U.S. e-cigarette market could soon turn out to be a golden goose for the company.

With a population of over 330 million, growing half a percent each year, earning a high median income relative to the rest of the world, the U.S. will likely be PMI’s most exciting market over the next decade. Probably the most important aspect of PMI’s Swedish Match acquisition was gaining control over the Zyn-maker’s vast distribution network, covering gas stations, 7-Elevens, Krogers, Harris Teeters, Walgreens, and many other retailers across the country. Having bought back from Altria the right to sell IQOS in the U.S. (starting in 2024), Swedish Match’s distribution network sets PMI up nicely to introduce its IQOS products to American smokers and e-cigarette users, assuming management can secure PMTA authorizations from the FDA for its new products.

If PMI’s success in Europe is any indication, it would not be surprising to see PMI take share from existing combustibles in the U.S. over the next several years. And if the FDA finally gets around to removing non-PMTA-authorized products from store shelves, those few companies left standing (e.g., Altria, BTI, PMI, and Imperial) will likely monopolize the American e-cigarette market much like they do the combustibles market today.

Thanks for reading.

Other pieces in this series on PMI:

The New and Improved Philip Morris International

Philip Morris International: Europe

Philip Morris International: Middle East & Africa

This piece is for informational purposes only. You should not construe anything herein as investment, financial, legal, tax, or other advice. Nothing contained in this piece constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments.

All content in this piece is for general informational purposes only and does not address the circumstances of any particular reader. Nothing in this piece constitutes professional and/or financial advice, nor does it constitute a comprehensive or complete statement of the matters discussed. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other content in this piece before making any decisions based on such information or other content.