Philip Morris International: Capital Allocation

Philip Morris International: Capital Allocation

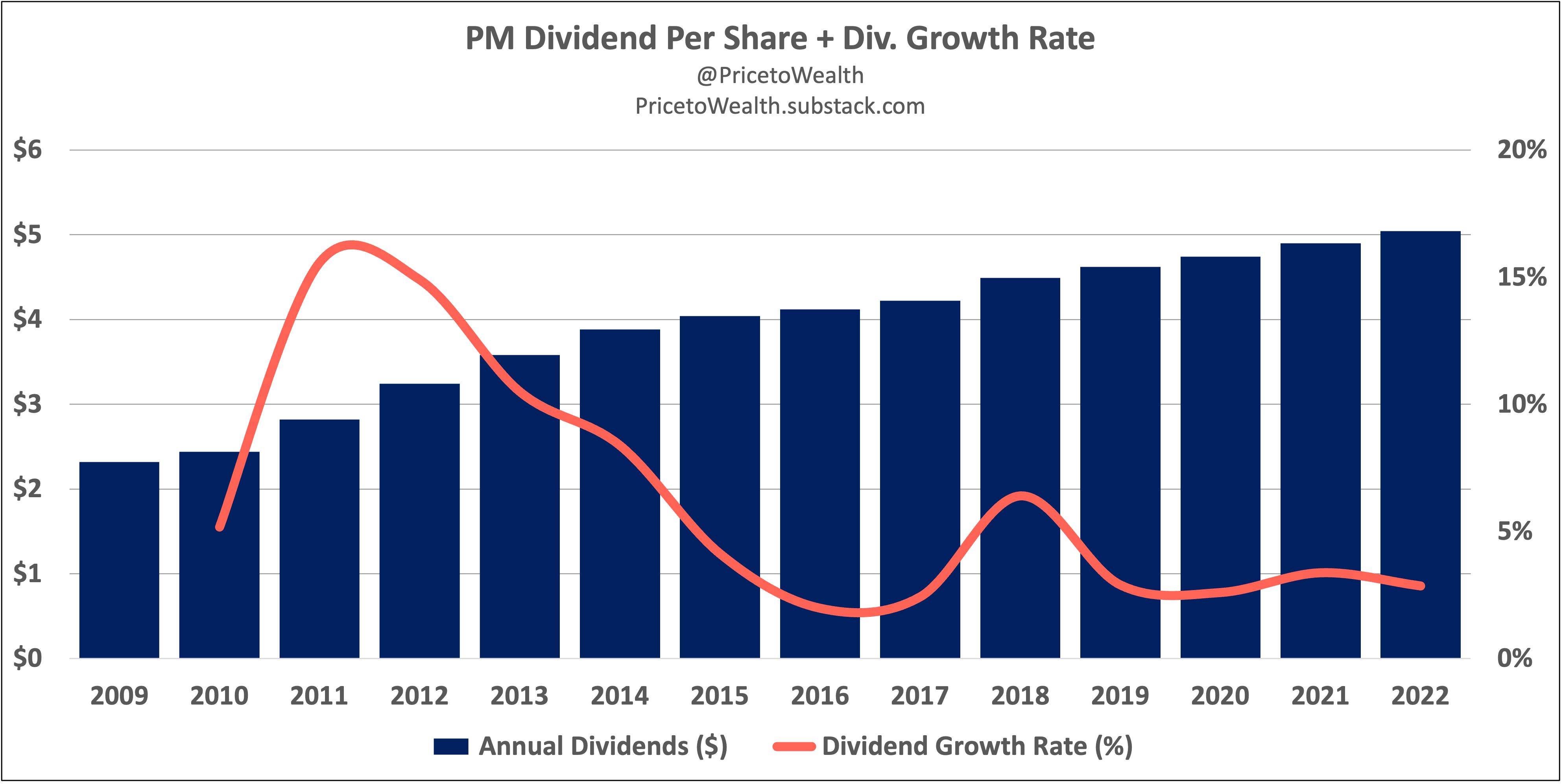

PMI has returned over $120 billion to shareholders since Altria spun it off in 2008.

Like its U.S.-focused counterpart, PMI management prioritizes returning capital to shareholders. Management has returned just over $120 billion to shareholders via dividends and buybacks from 2009 to 2022. Its market capitalization today is ~$150 billion.

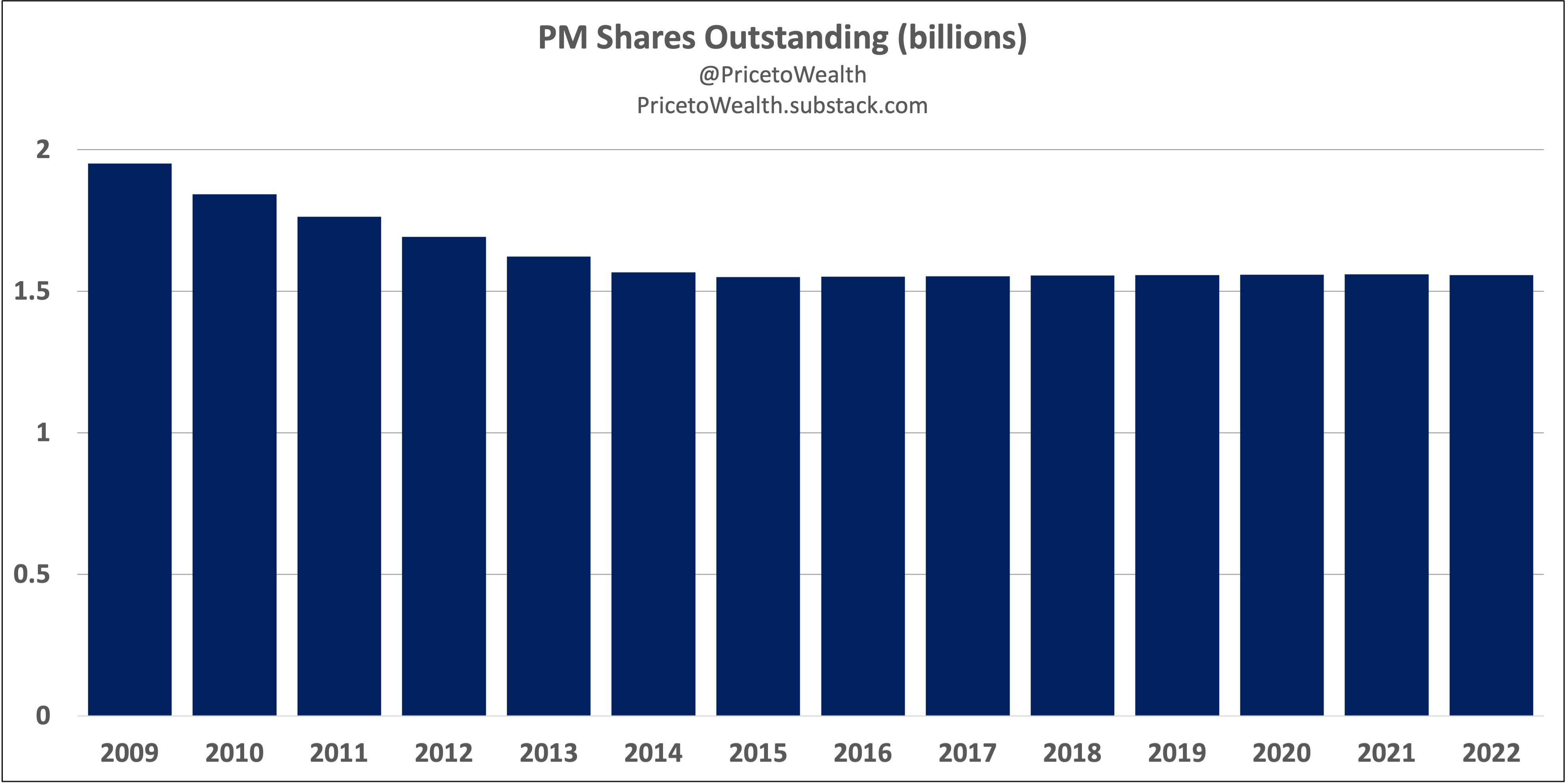

So from 2009 to 2022, management has dished out ~80% of the value of the company to shareholders (the company reduced its share count by over 20% between 2009 and 2022).

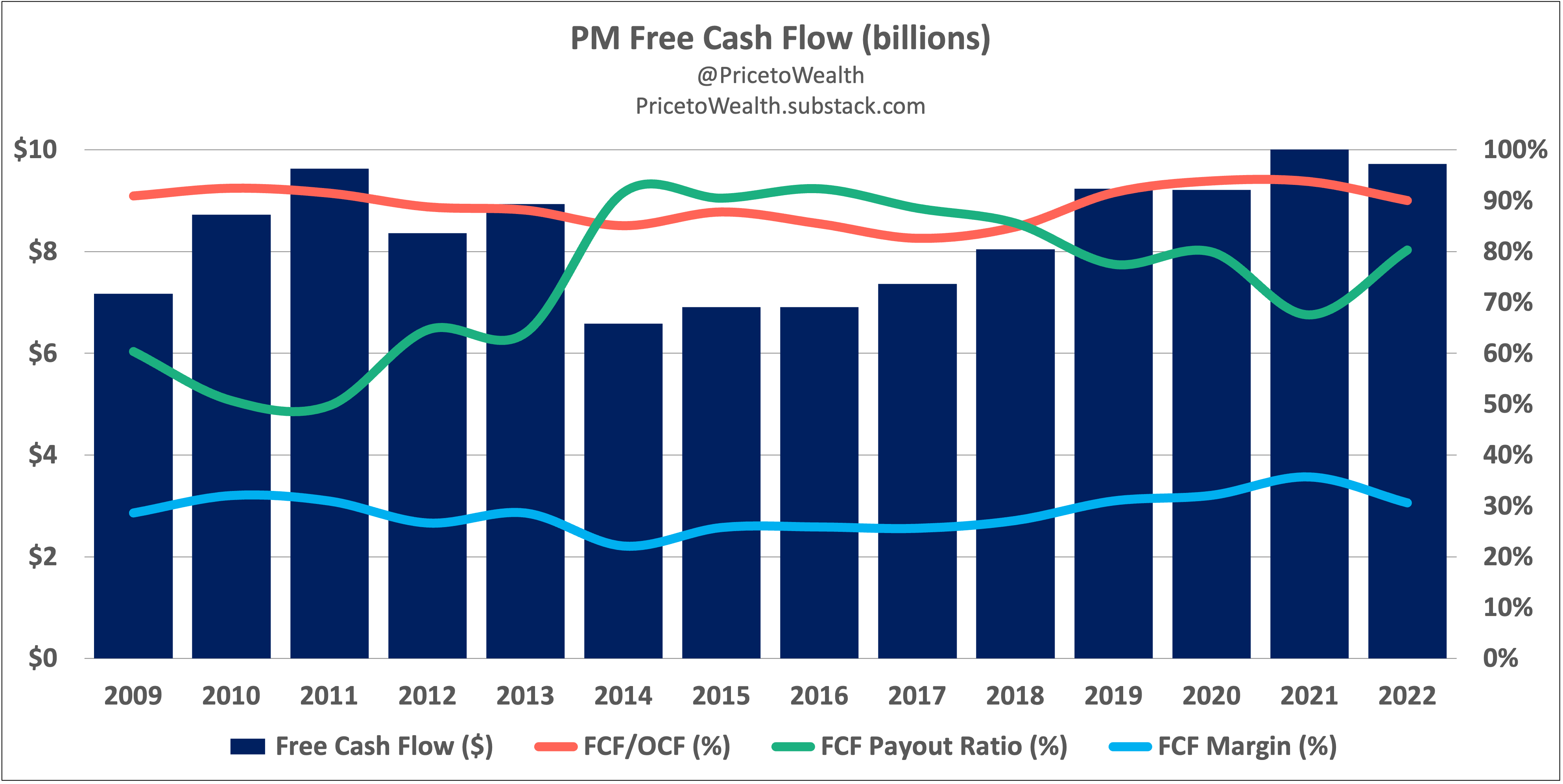

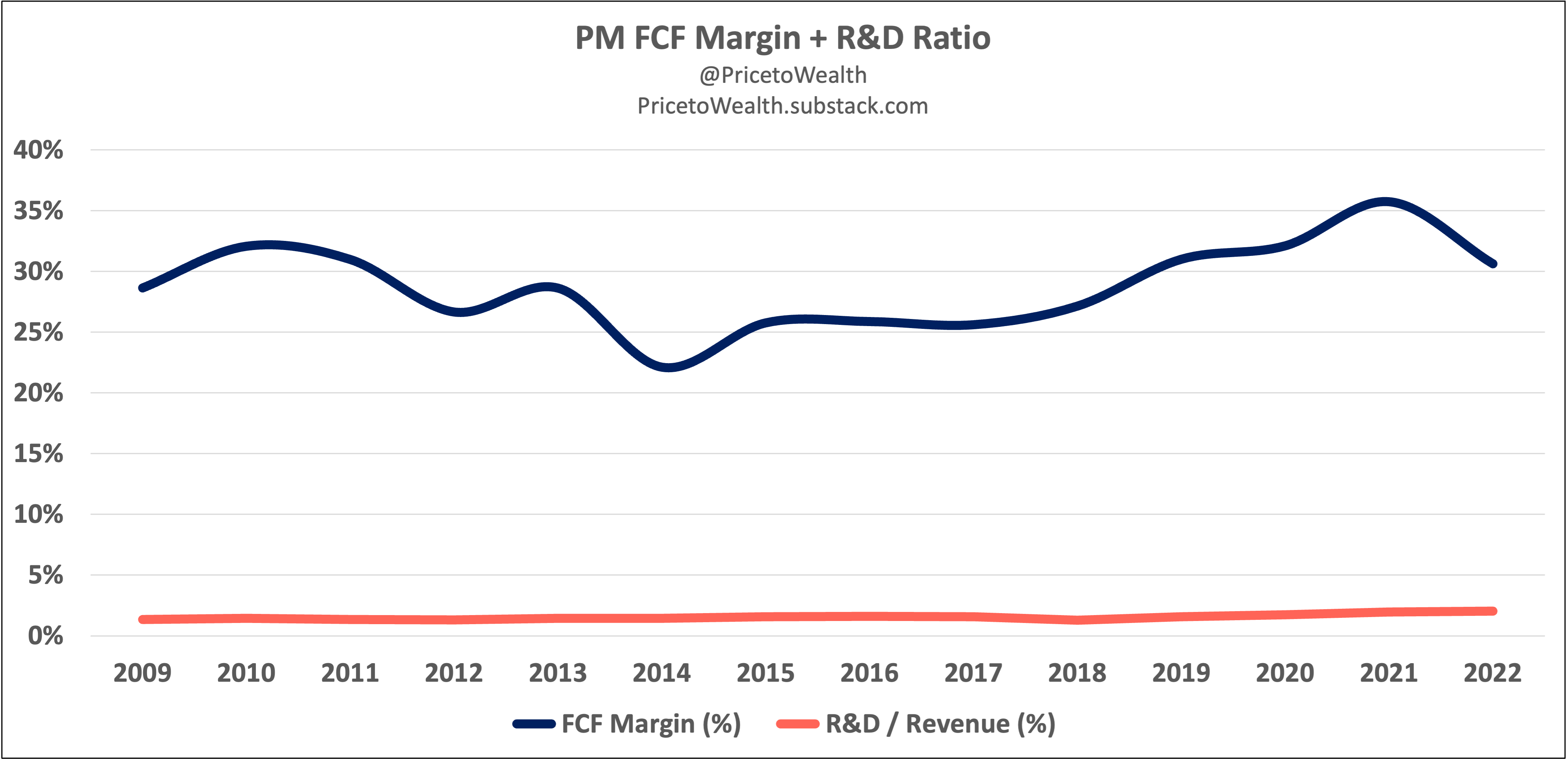

Since 2009, PMI’s average annual spend on maintaining, buying, and improving its fixed assets — properties like factories and equipment — has amounted to ~11% of operating cash flow. The business has converted almost 90% of operating cash flow to free cash flow for over almost fifteen years. Altria, on the other hand, has on average converted over 95% of its OCF to FCF.

PMI has had higher capital expenses compared to Altria because its business is global. While Altria only has to spend on factories and equipment in the U.S. (Altria’s annual report lists just two manufacturing facility locations — Richmond, VA, and Nashville, TN), PMI has to foot the bill for over fifty manufacturing facilities located all over the world.

Indeed, Altria’s management team has highlighted the concentration risk inherent in its reliance on just a few manufacturing facilities.

So while PMI’s capital expenses are higher than Altria’s, its business isn’t exposed to the same sort of concentration risk with respect to manufacturing capabilities.

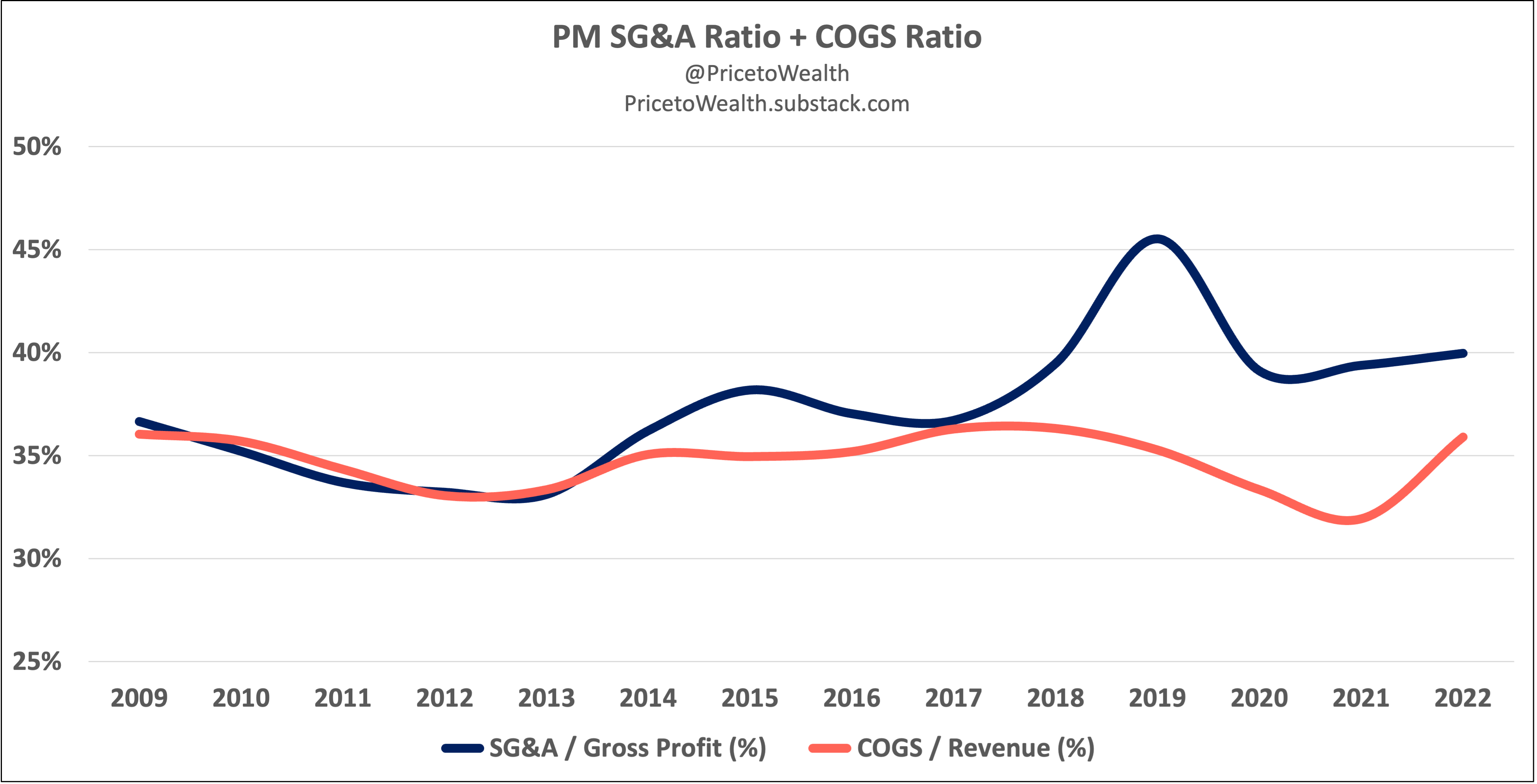

PMI’s ability to generate substantial free cash flow depends in large part on management’s control over costs. While PMI’s revenue is up ~27% from 2009 to 2022, its cost of materials and labor (COGS) has increased just as much.

And while gross profits are up 27% over the same period, PMI’s SG&A (salaries, rent, distribution costs, etc.) has increased 38%.

In these two areas (COGS and SG&A), PMI has been less efficient than Altria. These differences are due in part to PMI’s sprawling, global operations compared to Altria’s sole focus on one geographical region (the U.S.).

PMI has also invested heavily in new nicotine delivery technologies. That R&D accounts for just 2% of revenue.

Thanks for reading.

Other pieces in this series on PMI:

This piece is for informational purposes only. You should not construe anything herein as investment, financial, legal, tax, or other advice. Nothing contained in this piece constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments.

All content in this piece is for general informational purposes only and does not address the circumstances of any particular reader. Nothing in this piece constitutes professional and/or financial advice, nor does it constitute a comprehensive or complete statement of the matters discussed. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other content in this piece before making any decisions based on such information or other content.

PM has a great story with IQOS, Zyn, and soon its entry into the lucrative US market. My concern is that EPS growth has been low. Adjusted EPS has increased from $5.53 in 2013 to an expectation of $6.23 in 2023. (To be fair I’m cherry picking the dates.) But I’m always skeptical at the many IB analysts who keep writing PM is a double digit EPS growth story.